The European Union’s new Corporate Sustainability Reporting Directive comes into force from January 1st 2025 – it has the potential to transform sustainability reporting around the world.

The Corporate Sustainability Reporting Directive (CSRD) follows a long line of European Union policies intended to push economic and investment activity towards more sustainable outcomes. With a refreshed, holistic vision, the new directive aims to bring the ‘S’ in ESG into focus, highlighting the need for health and wellbeing alongside environmental measures.

Almost eight in ten businesses have not started preparing for the new ESG requirements, according to ESG compliance provider, VinciWorks. The survey of 175 ESG and strategy leaders revealed only half of respondents believe their business would fall within the new EU mandate.

More stringent than previous policies, and with a larger reach, what does the CSRD involve, and why could this policy be a gamechanger in global ESG reporting standards – and performance?

What is the CSRD?

The CSRD requires companies to report on the impact of corporate activities on the environment and society and requires the audit (assurance) of reported information. The CSRD replaces the Non-Financial Reporting Directive (NFRD), which only covered the disclosure requirements for about 11,000 EU companies. In contrast, the CSRD will require nearly 50,000 companies to enhance their reporting around sustainability. The NFRD was never mandatory.

Why is the CSRD being introduced?

The purpose of the CSRD is to provide investors and businesses with more information about the sustainability of companies operating in the EU, that is timely, consistent and comparable. The CSRD strengthens the existing rules on non-financial reporting introduced by the NFRD, which are no longer aligned to the EU’s transition towards a sustainable economy.

Ultimately, European regulators hope that this higher disclosure bar will act as a best practice model in ESG disclosure. The idea is that the CSRD will cause companies across global markets to follow the more stringent disclosure standards set by the EU to keep pace with best practices.

Which companies will fall under the CSRD?

CSRD will apply to all companies listed on regulated markets in the EU (apart from listed micro-enterprises), and large companies. The rules will cover both public and private business that satisfy two of the following criteria:

- Have more than 250 employees

- Have net turnover of more than $44.51 million

- Have a balance sheet of more than $22.25 million

Why will the CSRD impact companies based outside the EU?

There are three key ways in which non-EU groups or companies will be affected by the CSRD: if they have securities listed in the EU, have significant activity in the EU, or are parent companies of in-scope EU subsidiaries. Plus, the CSRD is already becoming the default sustainability disclosure regulation for large global companies as companies with significant business in Europe have to adhere to the rules Europe sets down.

What is the timeline for the CSRD?

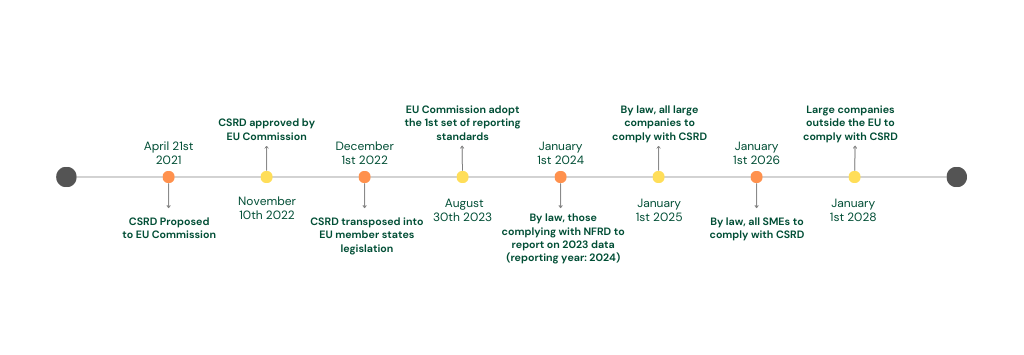

The CSRD was adopted by the EU Council in November 2022. EU companies already subject to the NFRD will have to begin compliance with the CSRD, which means reporting in 2024. Those for whom this reporting will be new, including companies outside the EU, have until 2025 to begin complying.

Companies that meet the reporting requirements will have to submit their first report of aligning with CSRD by Jan. 1, 2025. Smaller and medium-sized entities (SMEs) won’t have to comply with the rules until January 2026.

What is covered by the CSRD?

The CSRD reporting format will use European Sustainability Reporting Standards (ESRS) as a framework for how companies will be required to report. In essence, the CSRD is the law mandating ESG reporting, and the ESRS will act as guidance for how to best comply.

There are 13 ESRS metrics which have been selected to expand on ESG reporting boundaries to encompass the entire value chain, increasing the scope and granularity, bringing a refreshed focus to people, health, and wellbeing. The 13 ESRS metrics will be divisions of four broad categories:

Environmental (5 topical standards, E1-E5)

- E1: Climate change

- E2: Pollution

- E3: Water and marine sources

- E4: Biodiversity and ecosystems

- E5: Resource and circular economy

Social (4 topical standards, S1-S4)

- S1: Own workforce

- S2: Workers in the value chain

- S3: Affected communities

- S4: Consumers and end users

Governance (2 topical standards, G1-G2)

- G1: Governance, risk management, and internal control

- G2: Business Conduct

Cross-cutting Standards (ESRS1 – ESRS2)

- ESRS1: General reporting principles

- ESRS2: Strategy, governance, materiality, and disclosure requirements

These standards are set to be expanded, with sector-specific standards releasing over the next few years.

What will be the wider impact of the CSRD?

CSRD is not only expanding reporting requirements; the Directive will also drive all companies to eventually adopt a continuous ESG reporting system. With only 23% of businesses confirming they have starnted preparing for the new mandate, according to VinciWorks, fast understanding, measurement, and communication of ESG measures will be a top priority.

The new legislation focus will reduce the ability to greenwash ESG claims, and assure investors that companies place ESG as a priority alongside financial reporting. However, half of the VinciWorks respondents shared concern that the most significant challenge will be collecting data from supply chains on emissions and nature.

“Organisations that prioritise preparation over procrastination are better positioned to enact policies and procedures that ensure seamless compliance,” said VinciWorks’ director of learning and content Nick Henderson-Mayo.

“CSRD will push forward the adoption of sustainability and wellbeing in a way we haven’t yet seen”.

Driving large-scale change, the CSRD will push forward the adoption of sustainability and wellbeing in a way we haven’t yet seen. Crucially, the renewed focus on the ‘S’ in ESG will require companies to effectively translate their wellbeing impacts. This means demonstrating a drive for workforce health, welfare and community protection is key, and should be delivered with equal precision to environmental reporting.

How does the CSRD impact the built environment?

For building managers, owners and operators, CSRD means ensuring property management is scrutinised inline with ESG standards. Building operations and workforce structures will need to ensure credible reporting of physical, mental, and environmental health in order to align with valuation priorities and development opportunities.

Where can I learn more?

For more information, visit EC Corporate Sustainability Reporting.

______

Content Coms specialises sustainability comms strategies, ESG road-mapping and storytelling for a wide range of businesses – including UK & global manufacturing companies. Got a project? Let’s talk.